What You Need To Know About Small Business Credit Scores

The Right Equipment, Right Now

Getting the necessary equipment when you need it most may enable your small business to better compete at landing new projects. Some businesses reach a plateau and need to invest in their equipment in order to grow and become more profitable. Whether it’s new technology, machinery, vehicles or office furniture, increasing your company’s capability is essential for growth.

With Risk Comes Reward

Purchasing new or used equipment may be the next step, but not without risk. Most small businesses keep a sharp eye on their cash flow and may not wish to spend it on equipment. It turns out that some equipment finance options don’t require a big outlay and are eligible for Section 179 tax deductions which are very generous. Terms may be flexible which enables friendly month payments.

Set yourself for business success by creating relationships with financial providers like Commercial Capital that may help you get the machines you need to compete so you can reach the next level.

Boost Your Small Business Credit Score

Is your Small Business Credit Score causing problems when seeking lines of credit? Are you a small business owner who’s getting the cold shoulder from traditional lenders? Are banks insisting on terms you find downright unfriendly? Traditional banks are tightening credit as the Feds continue to raise rates with no end in sight for 2023. As you know, a poor credit score is not doing you any favors. Taking steps to improve your score will payoff down the road.

Like a personal credit score, a business credit score measures the level of risk you pose to a potential lender. Unlike personal credit scores, most of which adhere to the FICO model, business credit scores don’t follow an industry standard. Understanding the three major business credit bureaus will give you the insight necessary when seeking equipment financing.

Three Major Bureaus

- Dun & Bradstreet

- Equifax

- Experian

Each uses different methods to compile and monitor business credit scores. All calculate their scores using different criteria and use different number ranges. For example:

Dun & Bradstreet

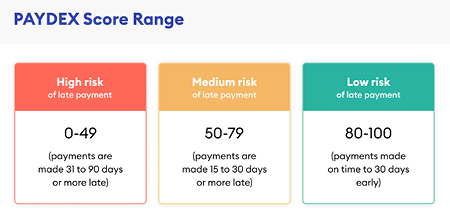

Dun & Bradstreet uses a proprietary Paydex Score that is based on payment data. Of the top three, D&B is the only credit bureau that focuses solely on business credit. Based on your established supplier/vendor relationships, you can develop an acceptable score by a history of prompt payments. You should know, paying on time will only earn you a score of 80. Here’s the kicker, you need to pay early to get a perfect PAYDEX score of 100. A history of paying early gets you the highest rating which is reserved for businesses that pay 30 days earlier than terms demand. D&B also looks at public records, industry data and other historical data in your D&B profile to compile their credit scores.

Dun & Bradstreet uses a proprietary Paydex Score that is based on payment data. Of the top three, D&B is the only credit bureau that focuses solely on business credit. Based on your established supplier/vendor relationships, you can develop an acceptable score by a history of prompt payments. You should know, paying on time will only earn you a score of 80. Here’s the kicker, you need to pay early to get a perfect PAYDEX score of 100. A history of paying early gets you the highest rating which is reserved for businesses that pay 30 days earlier than terms demand. D&B also looks at public records, industry data and other historical data in your D&B profile to compile their credit scores.

Delinquency Predictor Score: This measures the likelihood of a business to pay their bills late or go bankrupt over the next 12 months.

Failure Score: This is designed to forecast the probability that a business will seek legal relief from creditors or go out of business and leave creditors unpaid in the next 12 months.

Supplier Evaluation Risk Rating: This forecasts the likeliness that a business might stop delivering its goods and services over the next 12 months.

D&B Rating: This looks at a company’s financial statements and other public information to create an overall rating for a business’s creditworthiness. Ensure your D&B profile includes accurate, up-to-date financial statements which may greatly improve your D&B rating.

Credit Limit Recommendation: Creditors and banks review this recommendation, which is based on a business’s size, industry and payment history.

Equifax

Data collected by the Small Business Finance Exchange (SBFE) is combined into a report. Equifax uses three assessments to rate businesses:

Data collected by the Small Business Finance Exchange (SBFE) is combined into a report. Equifax uses three assessments to rate businesses:

Payment Trend and Payment Index: This examines your payment history over the past 12 months and how it compares to industry norms.

Equifax Business Credit Risk Score: This evaluates the likelihood your business will become severely delinquent.

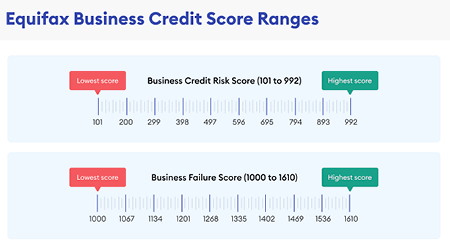

Equifax Business Failure Score: This measures the chance your business will close through either formal or informal bankruptcy over the next 12 months. The range is from 1000 to 1610 – lower scores indicate higher risk.

Experian

Experian gathers credit information from suppliers and lenders. In addition to examining credit history, Experian calculates its score by checking public records for liens, judgments and bankruptcies. Demographic information including how long you’ve been in business, the kind of business you’re in and the size of your business is included in its assessment. They collate information available in the public record, including legal filings from local, county and state governments, as well as information from credit card companies, collection agencies, corporate financial information and other databases.

Experian gathers credit information from suppliers and lenders. In addition to examining credit history, Experian calculates its score by checking public records for liens, judgments and bankruptcies. Demographic information including how long you’ve been in business, the kind of business you’re in and the size of your business is included in its assessment. They collate information available in the public record, including legal filings from local, county and state governments, as well as information from credit card companies, collection agencies, corporate financial information and other databases.

They examine:

- Number of credit transactions

- Outstanding balances

- Payment habits

- Available credit you use

- Details of any current liens

- Judgments or bankruptcies

- Time in business

- Size of your business

- Standard Industry Classification (SIC) codes

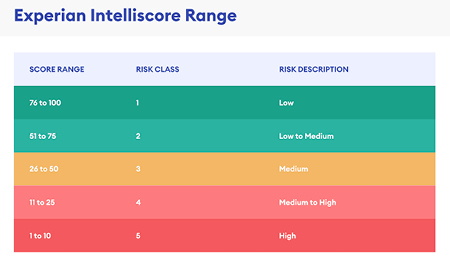

These data points combine to inform your Experian Business Credit Score which ranges from 0 to 100 and lists as follows:

- 0-15: High Risk

- 16-30: Medium Risk

- 31-80: Good Credit

- 80-100: Excellent Credit

In addition, Experian generates a Financial Stability Risk Rating that measures the risk of a company’s going into bankruptcy or severe financial distress in the next 12 months. This rating ranges from 1 to 5, with lower ratings indicating lower risk.

Because information is collected from both trade data and bank data, Experian’s business credit report may be considered the most balanced of the big three. Regardless of whether you rely primarily on trade credit for capital or access capital from a bank, Experian will have data on your business.

Your Partner For Growth

Unlike traditional banks, Commercial Capital makes it easier for you to acquire capital equipment with structured payments and 100% financing for the equipment you need.

Many lenders take a cookie cutter approach to financing. A flexible lender listens to your story and asks insightful questions to understand your business goals. You want a lender that acknowledges that character is not determined by a credit score. When evaluating cash flow, we want to understand your upcoming projects, jobs, and contracted work that may not yet show in your income stream. What is the potential monthly income for a new piece of equipment? This provides a clearer picture of your future cash flow. When structuring monthly payments, it’s important to consider how much income will result from revenue-generating equipment.

Share your story and we’ll show you how differently we think. We’ll design equipment financing solutions that helps you accomplish your business goals.

Fed Rate Hikes Continue Unabated

As interest rates continue upward, it’s important to lock-in with today’s rates while reaping the rewards as the economy recovers. At Commercial Capital Company, we have been able to turn uncertainty into opportunity by listening to our clients and providing them with financing solutions that help their small businesses grow.

Our funding application is a great way to start. Get pre-approved today for your next equipment purchase.

We’re a Veteran Owned Business.

We proudly support our nation’s veterans. Find us on Veteran Quote.

Contact Us

13910 W 96th Terrace

Lenexa, KS 66215

Toll Free: (800) 878-8053

Direct: (913) 341-0053

E-mail: sales@ccckc.com